Digital Wallets vs Traditional Banks: Which Is Better For Your Family's Financial Future?

- Carl Johnson

- Dec 20, 2025

- 6 min read

Look, we need to talk about something that's been keeping us up at night here at Storehouse Grocers - and honestly, it should be keeping you up too. The way families manage their money is changing faster than we can keep up, and we're all caught between these old banking systems and these new digital wallet things, and nobody's really explaining what this means for our actual lives, our actual families, our actual communities.

We've been watching our neighbors struggle with this choice, and we've been struggling with it ourselves because... well, because we're building something different here. We're trying to create financial empowerment through the Storehouse Wallet, but we also know that most families still need traditional banks for the big stuff, right? And this tension - this push and pull between old and new - it's real, and it's affecting how we build wealth in our communities.

Why This Choice Matters More Than We Think

Here's the thing - and we're being completely honest here because this community deserves honesty - traditional banks have been serving some families really well for decades. But have they been serving ALL families well? Have they been serving families who live paycheck to paycheck, families who can't maintain minimum balances, families who need to send money to relatives in other countries every month?

We see it every day in our store. Families choosing between paying bank fees and buying groceries. Families waiting days for paychecks to clear while their kids need lunch money today. Families who can't even open bank accounts because of past financial struggles, so they're paying check-cashing fees that eat up money that should be going toward building their future.

And then we have these digital wallets promising instant everything, lower fees, easier access... but are they actually delivering on those promises? Are they giving families the full range of financial services they need to build generational wealth?

Traditional Banks: The Foundation We've Always Known

Let's be real about traditional banks for a minute. They've been the backbone of family financial planning for generations, and there are reasons why your grandparents trusted them, reasons why they still matter today.

When we think about building long-term wealth - and we think about this constantly because community wealth-building is literally what we're about - traditional banks offer things that digital wallets just... don't. Savings accounts that earn interest. Loans for buying homes. Investment services. Insurance products. The full ecosystem of financial services that families need to move from surviving to thriving.

And that FDIC insurance? That $250,000 protection per account? That's not just a number - that's peace of mind. That's knowing your emergency fund is actually safe when emergencies happen. Because they will happen. They always do.

But here's where we get frustrated with traditional banking, where we see the gaps that are hurting our community... the speed. The fees. The barriers to entry. When your bank takes three business days to process a transfer and charges you $35 for an overdraft, that's not serving working families. That's extracting wealth from communities that can't afford to lose it.

We've watched neighbors get turned away from bank accounts because of past financial mistakes. We've seen families pay hundreds of dollars in fees every year just for the privilege of having their money held by an institution. And international transfers? Forget about it. The fees are predatory, the speed is glacial, and families supporting relatives abroad get gouged at every step.

Digital Wallets: The Promise of Financial Democracy

Now digital wallets... this is where things get interesting, where we start seeing possibilities for actual financial justice. Because when we can move money instantly, when fees drop from dollars to cents, when families can open accounts without credit checks or minimum balances - that's when we start democratizing access to financial services.

The speed alone changes everything. Need to send money to help a family member with an emergency? Done in minutes, not days. Want to split a grocery bill with your neighbor? Instant transfer. Need to pay a contractor working on your house? No waiting for checks to clear.

And the accessibility... we're talking about financial services that work on any smartphone, that don't require you to take time off work to visit a branch, that don't judge your past financial mistakes or your current income level. This is financial inclusion in action.

But - and this is a big but that keeps us awake at night - most digital wallets are treating symptoms, not causes. They're making payments easier, but are they helping families build savings? Are they offering the loans families need to buy homes and start businesses? Are they providing the full range of financial services that create generational wealth?

And what happens when your phone dies? When the internet goes down? When the app crashes right when you need to pay for groceries? We're putting all our financial access into devices that break, systems that fail, technologies that exclude people who aren't digitally native.

The Reality Check We All Need

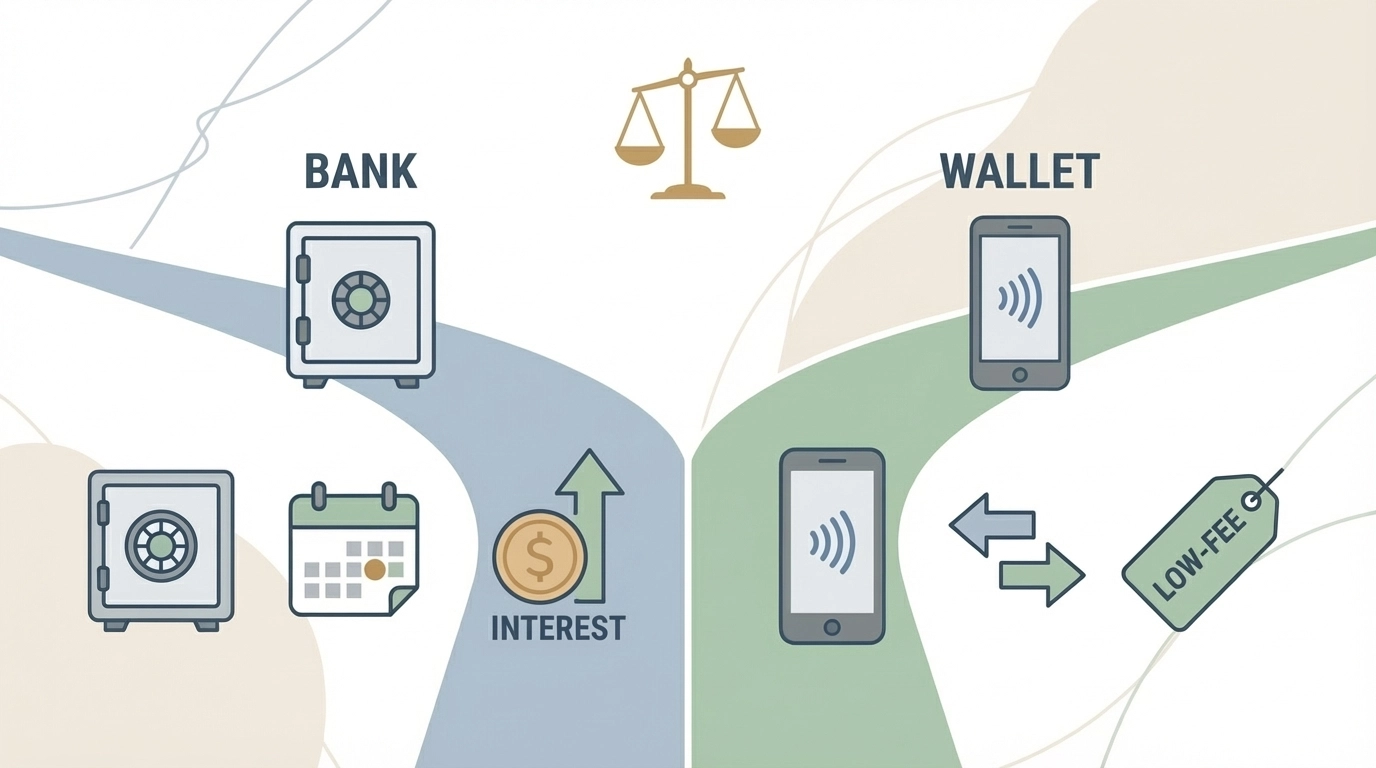

Here's what we've learned from watching families navigate this choice, from building our own financial services, from making our own mistakes and celebrating our own victories... this isn't really a choice between digital wallets OR traditional banks. This is about building a financial ecosystem that serves working families completely.

The families thriving financially in our community? They're using both. They're keeping their emergency funds and long-term savings in traditional banks where they earn interest and have FDIC protection. But they're handling their day-to-day transactions, their quick transfers, their small business payments through digital wallets where speed and low fees actually matter.

And this hybrid approach? It's not perfect. It requires managing multiple accounts, multiple apps, multiple relationships. It requires financial literacy that not everyone has access to. It requires smartphone technology and reliable internet that not everyone can afford.

What This Means for Your Family's Financial Future

So where does this leave us? Where does this leave your family? Where does this leave our community's financial future?

First, we need to stop thinking about this as an either/or decision. Your family's financial future probably requires both traditional banking stability AND digital wallet innovation. The question isn't which one to choose - the question is how to use both strategically to build the life you want.

Use traditional banks for the foundation: savings accounts, emergency funds, home loans, investment accounts, insurance. Use digital wallets for the flexibility: daily spending, quick transfers, international payments, small business transactions.

But more importantly - and this is why we're so passionate about what we're building here - we need financial services that actually serve working families. We need institutions that understand that financial empowerment isn't just about convenience or even just about lower fees. It's about building wealth, creating opportunities, strengthening communities.

Building Financial Justice Together

This is where Storehouse Grocers comes in, where our vision for community finance starts making sense. We're not just comparing digital wallets and traditional banks - we're building something different. Something that combines the stability families need with the innovation they deserve.

The Storehouse Wallet isn't trying to replace your bank account. It's trying to fill the gaps that both traditional banks and commercial digital wallets leave open. It's about financial services that understand food security, that support local economies, that build community wealth instead of extracting it.

Because here's what we know after years of serving this community: financial empowerment and food security go hand in hand. Families with stable, affordable financial services make different choices about food, about health, about their children's futures. Communities with locally-controlled financial institutions build wealth differently, more sustainably, more equitably.

We're building toward a future where families don't have to choose between speed and security, between convenience and comprehensive services, between innovation and institutional stability. We're building toward financial services that actually serve the people using them.

And we're doing this together. Not as customers and service providers, but as community members with shared stakes in each other's financial futures. Because that's how real change happens - not from the top down, but from the grassroots up, from neighbors supporting neighbors, from communities taking control of their own economic destinies.

The future of family finance isn't digital wallets versus traditional banks. It's community-controlled financial services that put families first, that build local wealth, that create the foundation for the more just economy we all deserve.

Join us in building that future. Your family's financial security - and your community's economic empowerment - depends on it.

Excellent article, Carl! Wondering if you know Malik Yakini, one of the originators of the Detroit Black Food Co-op...he is a dear friend and colleague of mine. If not, I'd be delighted to connect you to him.

Here's a YouTube which includes him speaking:

https://www.youtube.com/shorts/K5QTCbb4WDc

In solidarity and peace,

Diane Dodge (former colleague of yours on the St. Paul Ramsey FNC)