Blended Capital for Social Enterprises: A Practical Guide to Building a Capital Stack (with Grocery + Fintech Examples)

- Carl Johnson

- Jan 14

- 5 min read

So you're building something that matters, a grocery store in a neighborhood that traditional retail abandoned, a fintech tool that serves people banks won't touch, and you're trying to figure out how to fund it. Welcome to the weird and wonderful world of blended capital.

Here's the thing we've learned: there's no single "right" investor for community-focused ventures. There's a stack. And understanding how that stack works is probably the most important capital education you'll get as a social enterprise operator.

We're going to walk through what blended capital actually means, how the layers fit together, and share real patterns we're seeing in both grocery/food retail and fintech/financial inclusion. Because if you're building for community wealth? You need to speak this language.

What Is Blended Capital (And Why Should You Care)?

Blended capital is exactly what it sounds like, you blend different types of money together to fund something that traditional capital markets struggle to underwrite on their own.

Why does this matter? Because social enterprises operate in a tension. We're trying to build sustainable businesses and prioritize impact over maximum profit extraction. That math doesn't always pencil out for conventional investors who want 10x returns in five years.

So we layer capital sources with different risk tolerances and return expectations:

Philanthropic/grant capital that accepts zero or low returns

Mission-aligned debt that's patient and flexible

Community investment from people who believe in the mission

Equity or SAFE instruments for investors seeking returns plus impact

When you stack these right, you de-risk the whole structure. The grant money absorbs early losses. The patient debt gives you runway. The community notes build local ownership. And the equity layer becomes attractive because everything underneath it has already reduced the risk.

This is how you fund things that matter in places that need them.

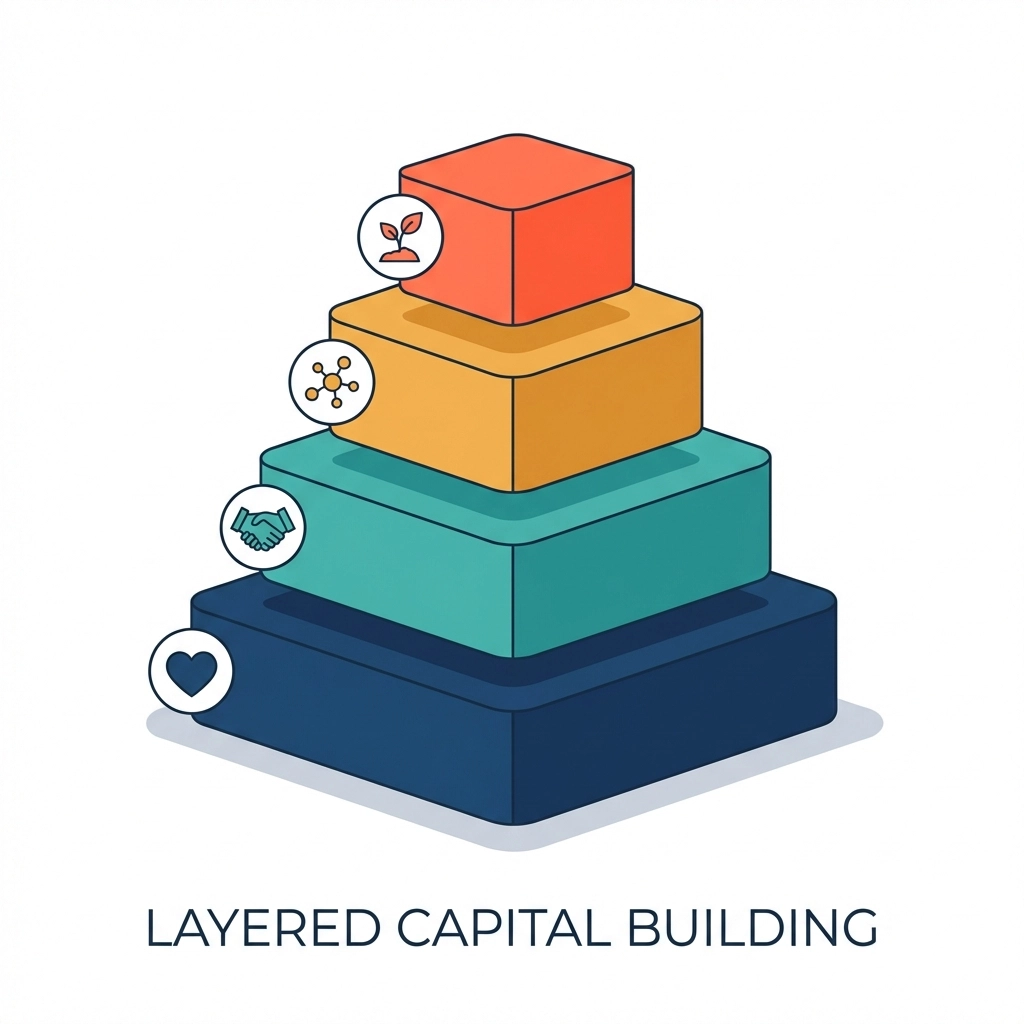

The Layers of a Capital Stack (Plain English)

Let's break down each layer because we see a lot of confusion here. Think of it like a building, foundation first, then structure, then the stuff people see.

Layer 1: Grants and Catalytic Capital (The Foundation)

This is your risk-absorbing base. Program-related investments (PRIs) from foundations, government grants, CDFI first-loss guarantees, these sources accept that they might not get paid back first (or at all) if things go sideways.

For grocery projects, this might look like a $50K-$150K PRI from a health-focused foundation or a Healthy Food Financing Initiative grant. For fintech, it could be a financial inclusion grant from a community development organization or a pilot program funded by a regional foundation.

The key insight: this layer makes everything above it possible.

Layer 2: Patient Debt (The Structure)

CDFIs (Community Development Financial Institutions), mission-aligned lenders, revenue-based financing, these sources want to get paid back, but they're flexible about how and when.

Think 5-7 year terms instead of 3. Think interest rates in the 4-8% range instead of 12-18%. Think covenants that actually make sense for a business serving low-income communities.

For a grocery store, this might be equipment financing or working capital with a 6-month grace period. For a fintech product, it could be development capital tied to user milestones rather than arbitrary dates.

Layer 3: Community Investment (The Ownership Layer)

Community investment notes, local investor programs, revenue-share agreements, this is where your neighbors and customers become stakeholders.

We love this layer because it does two things: it raises capital and it builds the kind of community ownership that makes your enterprise more resilient. Someone who invested $500 in your grocery store is going to shop there. Someone who bought into your fintech wallet is going to use it and tell their friends.

Typical community note terms we're seeing: $100-$5,000 minimums, 2-5% interest, 3-5 year terms.

Layer 4: Equity/SAFE (The Growth Layer)

This is where Wefunder and similar platforms come in. Investors who want ownership upside, who believe the business can scale, who see the capital stack underneath as de-risking their position.

The beautiful thing about a well-built stack is that by the time you get to this layer, you've already proven:

Foundation support (validation)

Debt capacity (revenue confidence)

Community buy-in (market demand)

That's a much easier conversation than "please take all the risk on an unproven concept."

How This Works in Grocery/Food Retail

Let's get specific. A community grocery store in a low-income neighborhood, food desert, limited options, real need, might build a stack like this:

Foundation layer ($75K-$200K):

Healthy food access grant from state program

PRI from regional health foundation

First-loss guarantee from CDFI

Patient debt layer ($100K-$300K):

CDFI term loan for equipment and buildout

Revenue-based financing for inventory

Community layer ($50K-$150K):

Community investment notes to neighbors

Local business sponsorships

Church and anchor institution investments

Equity layer ($100K-$500K):

Wefunder campaign to mission-aligned investors

SAFE notes with reasonable terms

Total raise: somewhere in the $400K-$1M+ range depending on scope. But here's what matters, no single source had to take on the full risk. The stack distributes risk according to each capital source's tolerance.

How This Works in Fintech/Financial Inclusion

Now flip to a digital wallet serving underbanked communities, SNAP integration, bill pay, no predatory fees. Different product, similar stack logic:

Foundation layer ($50K-$150K):

Financial inclusion pilot grant

Foundation PRI for product development

Government innovation fund participation

Patient debt layer ($75K-$200K):

CDFI working capital line

Revenue-based financing tied to active users

Community layer ($25K-$100K):

Community notes from early users and advocates

Credit union partnership investments

Anchor institution commitments

Equity layer ($150K-$750K):

Wefunder campaign positioning fintech + food retail integration

Impact investor SAFE notes

The fintech layer often requires more equity because software development is capital-intensive upfront. But the community and foundation layers still matter enormously, they prove demand and de-risk the technology bet.

Why Sequencing Matters More Than You Think

Here's where we see people get tripped up: they try to raise the equity layer first. Or they skip the community layer entirely. Or they treat grants as "free money" disconnected from the rest of the stack.

The sequencing matters because each layer validates the next:

Grants prove → foundations believe in your model Patient debt proves → lenders see revenue potential Community investment proves → your market wants this Equity becomes → a reasonable bet, not a charity case

When you walk into an equity conversation with the other layers already in place (or clearly mapped), you're not asking investors to take a leap of faith. You're showing them a structure where risk is distributed appropriately and multiple stakeholders have already said "yes."

That's investor-legible. That's how you build something fundable and impactful.

What We're Building (And Why We Think About This Daily)

At Storehouse, we're living this. We're building a community grocery store on West 7th in St. Paul and developing the Storehouse Wallet: a fintech tool designed to serve the same communities our store serves.

Two products. One integrated capital stack. Blended finance that makes sense because the grocery operation de-risks the fintech (proven community, existing users, real transaction data) and the fintech enhances the grocery (customer retention, financial inclusion, new revenue streams).

This isn't theoretical for us. It's operational. And we're learning something every week about how these capital layers actually work in practice: what foundations want to see, how CDFIs underwrite, what community investors care about, how to position for equity that doesn't extract from the community we're trying to serve.

Let's Talk About Your Stack

If you're an investor trying to understand how community retail and fintech capital structures work... or if you're an operator building something similar and want to compare notes... or if you're a foundation or CDFI thinking about where your capital fits in stacks like this...

We'd love to talk.

Book a call with us and let's dig into the details. How the layers connect, what we're learning, where the gaps are, and how mission-aligned capital can actually flow to projects that communities need.

Because this work matters. And we're figuring it out together.

Comments