Blended Capital for Food + Fintech: How Social Enterprises Fund What Banks Won't

- Carl Johnson

- Dec 20, 2025

- 5 min read

We've been thinking about this for months now, walking into bank after bank, presenting our vision for community-centered grocery stores that build wealth instead of extracting it... and getting the same polite rejection every single time. "Too risky," they say. "Unproven model," they explain. "Come back when you have three years of revenue."

But here's what we discovered: we're not alone in this struggle, and there's actually a whole world of funding that exists precisely because banks won't touch the stuff that matters most.

The Problem Banks Can't See (Or Won't Fund)

Traditional banks look at social enterprises like us - food + fintech combinations serving underbanked communities - and they see nothing but red flags. No credit history for our customers? Red flag. Serving SNAP recipients? Another red flag. Building technology that prioritizes community wealth over maximum profit extraction? The reddest flag of all.

But we keep asking ourselves: how do you fund innovation that banks fundamentally don't understand? How do you scale solutions for people that traditional finance has already written off?

The answer isn't trying harder to convince banks we're worthy... it's understanding that an entirely different funding ecosystem exists for exactly this reason.

Enter Blended Capital: The Funding Model Banks Fear

Blended capital - also called blended finance - is what happens when philanthropic money, government grants, and impact investors combine forces to de-risk investments that private markets won't touch alone. It's venture philanthropy meets social impact startup funding, and it's revolutionizing how we think about financing community-centered businesses.

Picture this simple diagram in your head: traditional bank financing sits on one end (low risk, low impact), pure grant funding sits on the other end (high impact, zero return expectation), and blended capital lives in that sweet spot in the middle where impact and sustainability meet.

We're talking about impact investing food systems where Community Development Financial Institutions (CDFIs) might provide a first-loss guarantee, a foundation offers patient capital at below-market rates, and private investors come in knowing their risk is dramatically reduced. Everyone wins: communities get the solutions they need, investors get reasonable returns, and the whole thing becomes sustainable and scalable.

Why Food + Fintech Needs This Funding Revolution

Here's something that keeps us up at night: 70-90% of all food in low-income areas gets produced, processed, and sold by small businesses, but these same businesses can't get traditional financing to save their lives. The financing gap? We're talking about $100 billion annually just in Africa alone.

And when you add fintech to the mix - digital wallets, micro-credit, financial literacy tools - traditional banks get even more nervous because now you're not just talking about food retail, you're talking about becoming a financial services provider to people they've systematically excluded.

But that's exactly why blended capital exists! It's designed to fund the innovations that banks won't touch but communities desperately need.

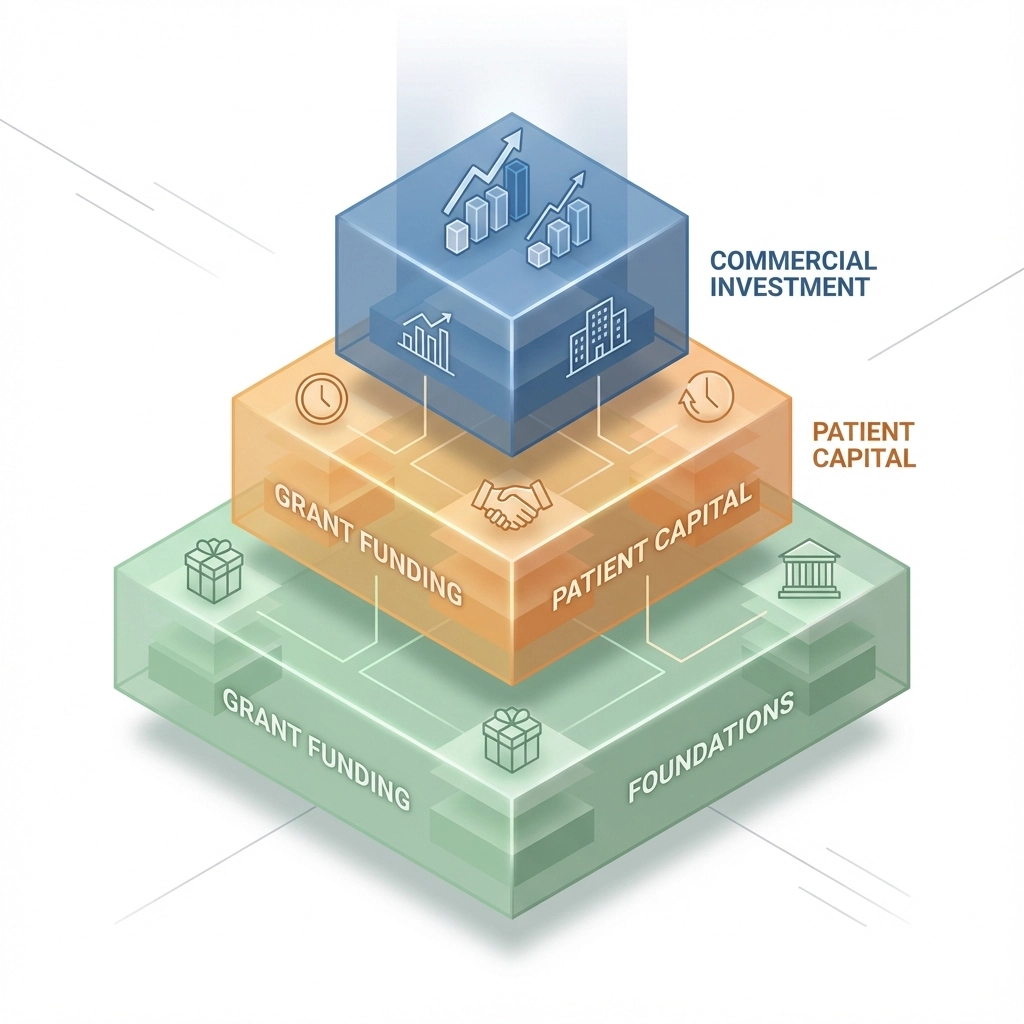

Breaking Down the Funding Stack

Let's get practical about how this actually works, because understanding the mechanics changes everything about how we approach funding:

Grants come first - these cover your proof-of-concept phase, your market research, your community engagement work. No payback required, but also limited in scale.

Patient capital comes next - this is debt or equity from impact investors who'll accept lower returns in exchange for measurable community impact. CDFIs excel at this kind of financing.

Commercial capital enters last - once the model is proven and de-risked, traditional investors jump in because now the numbers make sense and the risk profile fits their requirements.

The magic happens when you layer these together strategically, with each type of capital making the next level possible.

Venture Philanthropy Examples That Actually Work

We've been studying the International Finance Corporation's Blended Finance Facility, and honestly, it's giving us so much hope. They've been doing this for nearly 20 years, combining concessional funding from development partners with commercial funds to unlock private sector investment in exactly the kinds of businesses banks typically reject.

Take the Africa Agriculture and Trade Investment Fund - they're investing directly in agricultural supply chains with the explicit goal of increasing food security while strengthening income for people working in agriculture. They fund commercial farms, processing companies, cooperatives, AND the financial institutions that on-lend to small enterprises.

That's the model we need to replicate: comprehensive ecosystem thinking where the financing supports every level of the food system simultaneously.

Community Development Finance in Action

Here's what gets us really excited: CDFIs are already operating in this space, providing community development finance to businesses that look exactly like what we're building. They understand that serving underbanked communities requires different metrics, longer time horizons, and blended capital structures.

But we need more of them, and we need them working specifically in the food + fintech intersection. Because right now, there's this gap where CDFIs fund food businesses and other organizations fund fintech startups, but nobody's specifically funding the combination that creates real community wealth building.

The Technical Assistance Piece Nobody Talks About

One thing that makes blended capital so powerful - and this was a revelation for us - is that it often includes technical assistance funding alongside the investment capital. So you're not just getting money; you're getting capacity building, strategic support, systems development help.

When you're trying to build both a grocery operation AND a fintech platform AND a community wealth building initiative all at the same time... that technical assistance component becomes absolutely critical. You need advisors who understand food systems, others who understand financial services regulation, others who understand cooperative development.

Traditional bank loans definitely don't come with that kind of wraparound support.

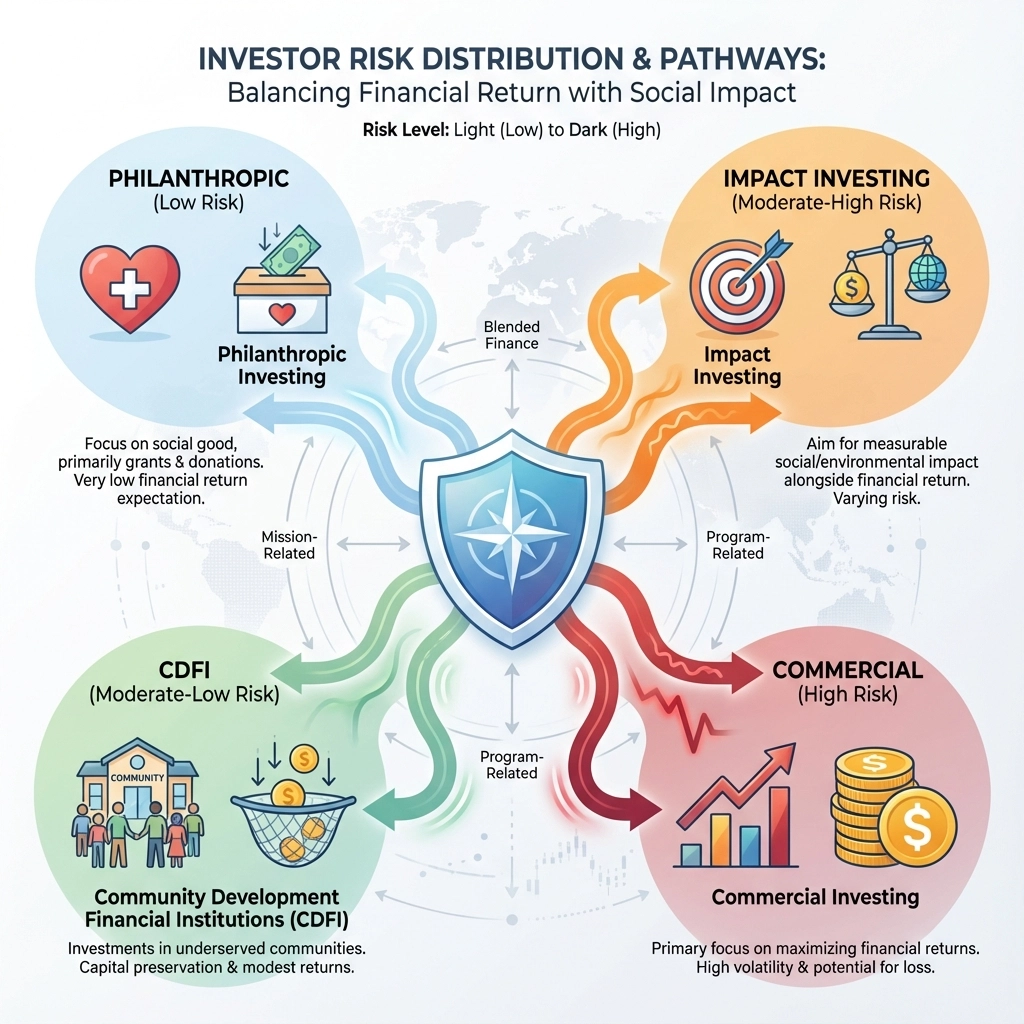

Risk Mitigation That Actually Works

The beauty of blended capital structures is how they handle risk distribution. Instead of trying to convince one investor to take on all the risk (impossible when you're doing something genuinely innovative), you're spreading different types of risk across multiple investor types who have different risk tolerances and different success metrics.

Philanthropic capital can handle the "proof-of-concept" risk. Impact investors can handle the "scaling in underserved communities" risk. CDFIs can handle the "lending to people without traditional credit" risk. And commercial investors can handle the "sustainable profitability" risk.

Each investor type gets the risk profile that makes sense for their mandate, and the whole structure becomes fundable where no individual piece would be.

What This Means for Social Impact Startup Funding

We're convinced that blended capital represents the future of social impact startup funding, especially for businesses operating at the intersection of basic needs and financial inclusion. The old model of "get venture capital or bootstrap forever" doesn't work when your customer base is systematically excluded from traditional financial systems.

But the new model - where patient capital from multiple sources combines to de-risk innovation for underserved communities - that's where the real breakthrough potential lives.

Building the Coalition We Need

This is where we need your help, honestly. We can't build this funding ecosystem alone, and neither can any individual social enterprise. We need a coalition of food fighters, fintech innovators, community development advocates, and impact investors all working together to prove that blended capital for food + fintech isn't just possible - it's essential.

The research is clear, the models exist, the need is overwhelming. What we're missing is the coordinated effort to scale these approaches specifically for businesses like ours that are trying to build community wealth through better food access and financial inclusion.

Are you working on something similar? Are you an investor interested in this space? Are you a community organization that could benefit from these models?

Because honestly, we're just getting started with this exploration, and we know we need partners, advisors, fellow travelers on this journey toward funding models that actually serve communities instead of extracting from them.

The banks may not understand what we're building, but the blended capital ecosystem does. And together, we're going to prove that community-centered businesses aren't just fundable - they're the future of sustainable economic development.

Join us in building this coalition of food fighters and fintech innovators. Because the communities we serve deserve so much better than what traditional finance has offered them, and blended capital gives us the tools to deliver it.

Comments